What is CCRIS and CTOS & How to Read CCRIS Report?

“Your loan is rejected because you have a bad CCRIS or CTOS record.” If you have ever heard these words from a bank officer, you are not alone. For many Malaysians, this is the moment they first begin to wonder what these systems actually are and how they affect their financial future.

To understand these reports, you must first understand how banks decide whether to approve your application. Financial institutions look primarily at your credit history—the record of your previous loan repayments. They want to know if you have been paying on time or if there have been delays or defaults. Generally, the more consistent you are with your payments, the better your credit history looks, and the higher your chances of success. Banks obtain this history through detailed credit reports produced by authorized agencies.

What is CCRIS? The Government’s Financial Ledger

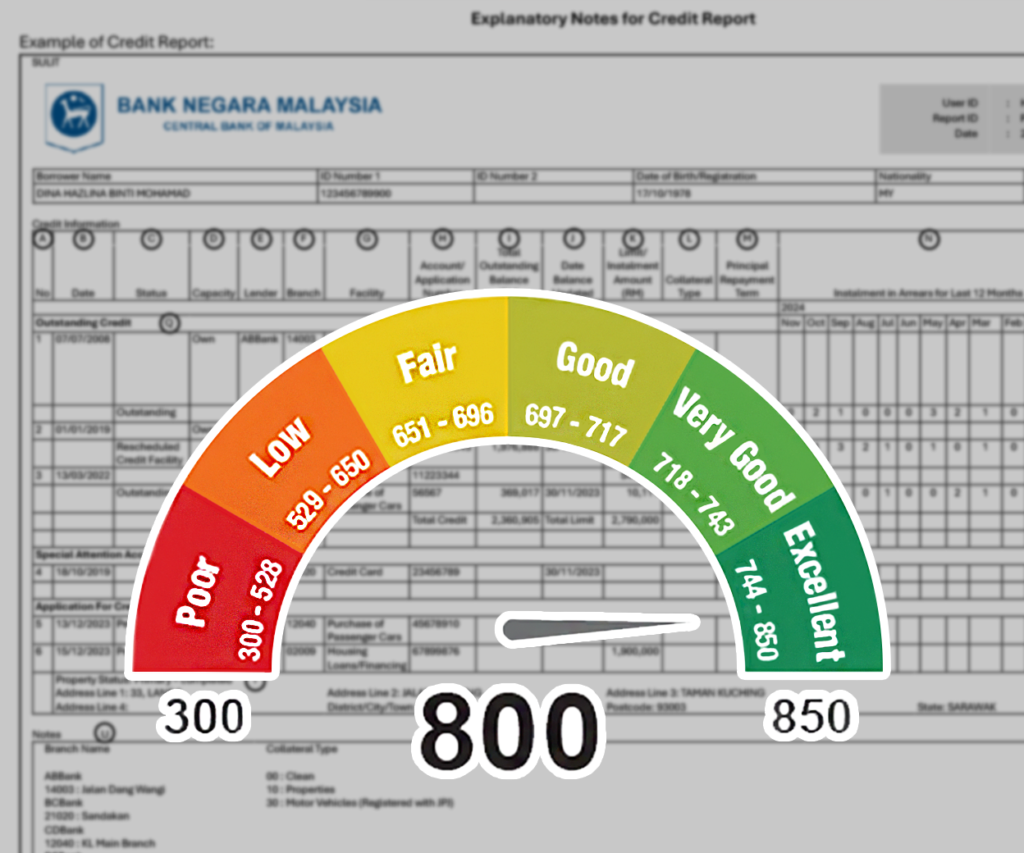

The Central Credit Reference Information System, commonly known as CCRIS, is a record maintained by the Credit Bureau of Bank Negara Malaysia. It is a centralized database that tracks your loan repayment behavior across the entire financial landscape.

A CCRIS report is incredibly detailed. It includes every loan you have with every financial institution in Malaysia, covering not just major banks but also non-bank institutions such as AEON Credit or PTPTN. When you look at your report, you will find your loan repayment history, your total outstanding balances, and your credit limits for the past 12 months.

What is CTOS? The Private Credit Database

While CCRIS is managed by the central bank, CTOS (Credit Tip-Off Service) is a private credit reporting agency. It serves a similar purpose but gathers its data from different sources.

Instead of just looking at bank loans, CTOS compiles information from public domains. This includes legal proceedings, bankruptcy notices, newspaper clippings, and even trade references from utility companies or telcos. If you have unpaid phone bills or have been summoned to court over a debt, it will likely show up on your CTOS report. By combining this public data with your banking history, CTOS provides lenders with a holistic view of you as a reliable borrower, which is the most effective way to ensure your future loan applications are approved.

The New Era of Credit: The Consumer Credit Act (CCA)

The way credit is reported in Malaysia is currently undergoing a significant shift with the introduction of the Consumer Credit Act (CCA). Set for full implementation between 2024 and 2025, this law establishes the Credit Monitoring Board (CMB) to regulate non-bank lenders that were previously less scrutinized.

This new legislation brings several important changes for consumers:

Regulating Non-Bank Lenders

Services like Buy Now Pay Later (BNPL) and various Koperasi (cooperatives) will now be subject to stricter oversight. This ensures that these lenders treat borrowers fairly and operate transparently.

Comprehensive Reporting

Because non-bank lenders will now be required to report data to systems like CTOS, your credit report will become much more complete. Every borrowing activity, whether it is a small BNPL purchase or a large cooperative loan, will be visible.

Encouraging Financial Literacy

While these rules mean banks and lenders will have stricter criteria for evaluating borrowers, the ultimate goal is to improve financial awareness. It encourages Malaysians to understand their rights and responsibilities before taking on new financial commitments.

By staying informed about your CCRIS and CTOS records, you can take active steps to solve financial struggles and position yourself for a more stable financial future.